Life science innovations have led to significant breakthroughs in healthcare and other sectors over the past decade. This has caught the attention of investors seeking alternative sources of returns in a low-yield and highly volatile market environment.

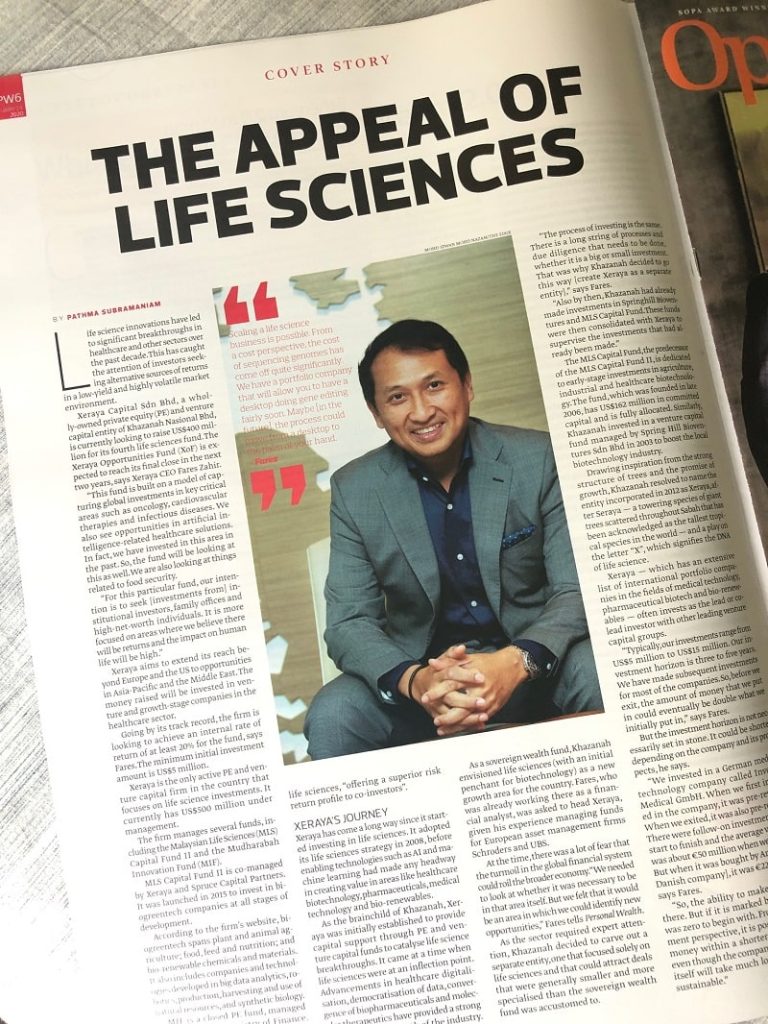

Xeraya Capital Sdn Bhd, a wholly-owned private equity (PE) and venture capital entity of Khazanah Nasional Bhd, is currently looking to raise US$400 million for its fourth life sciences fund. The Xeraya Opportunities Fund (XoF) is expected to reach its final close in the next two years, says Xeraya CEO Fares Zahir.

“This fund is built on a model of capturing global investments in key critical areas such as oncology, cardiovascular therapies and infectious diseases. We also see opportunities in artificial intelligence-related healthcare solutions. In fact, we have invested in this area in the past. So, the fund will be looking at this as well. We are also looking at things related to food security.

“For this particular fund, our intention is to seek [investments from] institutional investors, family offices and high-net-worth individuals. It is more focused on areas where we believe there will be returns and the impact on human life will be high.”

Xeraya aims to extend its reach beyond Europe and the US to opportunities in Asia-Pacific and the Middle East. The money raised will be invested in venture and growth-stage companies in the healthcare sector.

Going by its track record, the firm is looking to achieve an internal rate of return of at least 20% for the fund, says Fares. The minimum initial investment amount is US$5 million.

Xeraya is the only active PE and venture capital firm in the country that focuses on life science investments. It currently has US$500 million under management.

The firm manages several funds, including the Malaysian Life Sciences (MLS) Capital Fund II and the Mudharabah Innovation Fund (MIF).

MLS Capital Fund II is co-managed by Xeraya and Spruce Capital Partners. It was launched in 2015 to invest in biogreentech companies at all stages of development.

According to the firm’s website, biogreentech spans plant and animal agriculture; food, feed and nutrition; and bio-renewable chemicals and materials. It also includes companies and technologies developed in big data analytics, ro-botics, production, harvesting and use of natural resources, and synthetic biology.

MIF is a closed PE fund, managed on behalf of the Ministry of Finance. According to Xeraya’s website, the fund matches private sector investments in life sciences, “offering a superior risk return profile to co-investors”.

Xeraya’s Journey

Xeraya has come a long way since it started investing in life sciences. It adopted its life sciences strategy in 2008, before enabling technologies such as AI and machine learning had made any headway in creating value in areas like healthcare biotechnology, pharmaceuticals, medical technology and bio-renewables.

As the brainchild of Khazanah, Xeraya was initially established to provide capital support through PE and venture capital funds to catalyse life science breakthroughs. It came at a time when life sciences were at an inflection point. Advancements in healthcare digitalisation, democratisation of data, convergence of biopharmaceuticals and molecular therapeutics have provided a strong impetus for the growth of the industry.

As a sovereign wealth fund, Khazanah envisioned life sciences (with an initial penchant for biotechnology) as a new growth area for the country. Fares, who was already working there as a financial analyst, was asked to head Xeraya, given his experience managing funds for European asset management firms Schroders and UBS.

At the time, there was a lot of fear that the turmoil in the global financial system could roil the broader economy.”We needed to look at whether it was necessary to be in that area itself. But we felt-that it would be an area in which we could identify new opportunities,” Fares tells Personal Wealth.

As the sector required expert attention, Khazanah decided to carve out a separate entity, one that focused solely on life sciences and that could attract deals that were generally smaller and more specialised than the sovereign wealth fund was accustomed to.

“The process of investing is the same. There is a long string of processes and due diligence that needs to be done, whether it is a big or small investment. That was why Khazanah decided to go this way [create Xeraya as a separate entity],” says Fares.

“Also by then, Khazanah had already made investments in Springhill Bioventures and MLS Capital Fund. These funds were then consolidated with Xeraya to supervise the investments that had already been made.”

The MLS Capital Fund, the predecessor of the MLS Capital Fund II, is dedicated to early-stage investments in agriculture, industrial and healthcare biotechnology. The fund, which was founded in late 2006, has US$162 million in committed capital and is fully allocated. Similarly, Khazanah invested in a venture capital fund managed by Spring Hill Bioventures Sdn Bhd in 2003 to boost the local biotechnology industry.

Drawing inspiration from the strong structure of trees and the promise of growth, Khazanah resolved to name the entity incorporated in 2012 as Xeraya, after Seraya — a towering species of giant trees scattered throughout Sabah that has been acknowledged as the tallest tropical species in the world — and a play on the letter “X”, which signifies the DNA of life science.

Xeraya — which has an extensive list of international portfolio companies in the fields of medical technology, pharmaceutical biotech and bio-renewables — often invests as the lead or co-lead investor with other leading venture capital groups.

“Typically, our investments range from US$5 million to US$15 million. Our in-vestment horizon is three to five years. We have made subsequent investments for most of the companies. So, before we exit, the amount of money that we put in could eventually be double what we initially put in,” says Fares.

But the investment horizon is not necessarily set in stone. It could be shorter, depending on the company and its prospects, he says.

“We invested in a German medical technology company called Invendo Medical GmbH. When we first invested in the company, it was pre-revenue. When we exited, it was also pre-revenue. There were follow-on investments from start to finish and the average valuation was about €50 million when we invested. But when it was bought by Ambu A/S [a Danish company], it was €225 million,” says Fares.

“So, the ability to make a return is there. But if it is marked by revenue, it was zero to begin with. From an investment perspective, it is possible to make money within a shorter time horizon, even though the company or technology itself will take much longer to become sustainable.”

As life sciences cover a broad spectrum of industries, Xeraya hones in on companies that drive innovation across the value chain and enable that innova-tion to improve lives. “The reality is that healthcare as a whole will have inherent growth. The proliferation of the ageing population and the rise of disposable income has an impact on the quality of life. We have found that there is always going to be inherent, long-term growth in this segment,” he says.

“With life sciences being the focus, we are looking at a lot more than healthcare. Each of the other market segments that we have invested in is valued in the billions.”

Cost No Longer Barrier to Entry

The high cost was the main barrier impeding the sector’s growth in the past, says Fares, adding that it is “something that appears to be potentially dissipating”.

“Scaling a life science business is possible. From a cost perspective, the cost of sequencing genomes has come off quite significantly. We have a portfolio company that will allow you to have a desktop doing gene editing fairly soon. Maybe in the future], the process could move from a desktop to the palm of your hand.”

The global regulatory environment has been receptive to these changes. Regulatory reforms in the healthcare ecosystem, for example, is cited as one of the reasons the life sciences industry attracted more activity than ever last year, according to Venture Monitor, a quarterly report published by US-based Pitchbook and the National Venture Capital Association.

Data from the quarterly report suggests that more than half of the venture capital money invested in pharma and biotech each year since 2016 has been in the riskier angel, seed, Series A and Series B funding rounds.

To illustrate his point, Fares says new drug approvals by the US Food and Drug Administration (FDA) has been on the rise.”On top of that, the first-in-class type of drugs is taking a bigger percentage of the approvals.”

First-in-class drugs are those that use a new and unique mechanism of action for treating a medical condition, according to the US National Library of Medicine in one of its journals. Such products, despite being innovative solutions that offer new treatment options for patients, previously took months and sometimes years to obtain approvals.

“But now, the FDA has a new protocol to look at breakthrough technologies, which I expect will quicken the pace of approval and help drive the sector for-ward,” says Fares. “It is important even for us because in the past, we would probably have shied away from a medical or pharmaceutical technology that was deemed as first-in-class. The reason being that most of the companies we invest in have not reached self-sustainability yet and if we add the risk of breakthrough technologies to that observation, it gets riskier.”

As a result of this progress, Xeraya is close to sealing a deal with a company in the business of developing first-in-class types of products.

Investments With An Asian Twist

Many of the companies Xeraya invests in are located in the US. This is simply due to the fact that the country has one of the most developed ecosystems when it comes to the life science business.

“We have a few investments in Europe, but most are in the US. However, we take advantage of our Asian network as we have to add value to the portfolio companies and ensure that there is an Asian aspect to it,” says Fares.

“People are also looking at how we take advantage of Asia because whether we like it or not, there are billions of people here. Asia will have to deal with the challenge of a [growing] ageing population. The rising disposable income is also growing faster in this part of the world than it is in developed countries. The big companies themselves have a business model to see how they can capture the Asian market.”

One of Xeraya’s portfolio companies, San Francisco-headquartered InterVenn Biosciences, is an example of East meets West. The biotech company is developing cancer diagnostics using AI and next-generation mass spectrometry technique. It also employs deep learning to augment cancer diagnosis, biomarkers and target discovery. It has subsidiaries in Kuala Lumpur and Manila to foster biotechnology and drive AI adoption.

Mass spectrometry has been the primary analytical tool used in bioscience and medical research. InterVenn uses the tool to measure glycoproteomic markers that have been strongly linked to tumour development and progression.

“We do not need to have different technologies for different markets.What we do is look at the core of the technology and fit it to what works best for Asia. InterVenn, for example, does trials in the US, Malaysia and the Philippines,” says Fares.

“The CEO of InterVenn [Aldo Carrascoso] is a Filipino tech maven, who comes to work in a hoodie. It is very much like any other start-up, really.”

Cancer treatments and drugs aside, medical technology is another favourite of investors in the life sciences circle.

“In the last decade, we have seen impressive advances in robotics and improved imaging. In those lands of base technologies, we look at how it can be helpful in identifying solid tumours and cardiovascular diseases as well. But the trend going forward will be a combination of AI-enabled technology that links up with robotics and imaging to make the device more effective,” says Fares.

“The other combination is improving on tools that spot the problem and fix it at the same time. We have invested in a company called ViewRay Technologies, Inc. It combines MRI imaging with radiation therapy

“The current practice, if you have a solid tumour, is you would go to the physician to do a scan to locate the tumour and have few more scans after that to relatively treat it. But you cannot do so many of those CT scans because all that radiation is harmful.

“With this technology, because it is MRI, you can do it without doing much harm to the person. And with MRI, you can take many pictures at the same time that it becomes like a video. What happens is that you see and zap the tumour at the same time. It is very accurate because the physician can see it and be comfortable in giving as much radiation as needed to kill the tumour.

“Otherwise,there is a lot of guesswork. And as a physician, you would want to minimise errors as much as possible.So, you tend to not do as much as you should, and then the procedure takes too long.”

The bio-renewables segment is another area that has garnered interest of late, seeing that solutions to address more sustainable sources of energy are becoming more innovative but also more time- and cost-effective.

Driven by a range of environmental challenges such climate change and energy and material insecurity, a transition from the current fossil-based economy to a future bio-based one is expected to evolve progressively.

In line with this global initiative to muster capital to be reallocated to clean energy solutions around the world, Xeraya invested in LanzaTech Inc, which is working towards reducing global carbon dioxide emissions by 10%. It does this by recycling carbon from industrial off-gases; syngas generated from any biomass resource such as municipal solid waste, organic industrial waste and agricultural waste; and reformed biogas.

“Everybody is trying to reduce their carbon footprint. So, it is more about capturing that kind of carbon and producing something that provides value. LanzaTech has this technology where it genetically modifies microbes to basically chew on carbon monoxide and effectively throw out ethanol and produce enough clean fuel. The fuel was used on a Virgin Atlantic flight from Gatwick airport to Orlando,” says Fares.

“Carbon monoxide is produced by the steel industry. Chinese steel company Boasteel Group Corp is one of its big customers, and we expect there will be more. That is because China is trying to reduce its carbon footprint. So, it is a combination of the steel companies adopting the technology to help them meet those goals and LanzaTech being able to get the business?

It is also worth noting that Indian Oil Corp acquired a 4% stake in LanzaTech for US$20 million in 2018.

Fares says his team is looking out for more companies in the agricultural technology space.”One of the key themes coming out of there is the move away from chemicals to biology.”

In 2015, Xeraya — through its MLS Capital Fund II — invested in Provivi Inc, which has developed patented technology that dramatically reduces pest populations and minimises crop damage.

“It is able to produce pheromones at scale to control the proliferation of insects. The female insect secretes pheromones to attract the male insects — that is how they multiply. But if you have pheromones everywhere, it confuses the insects and disrupts their mating process,” he says.

A Critical View

Despite the nature of these novel therapies, these investments are not without risks. Apart from regulatory issues that could set these breakthroughs back, there are also risks associated with the sustainability of the company, says Fares.

“The question is, how do we manage these risks? For one, we take a more active approach because we are involved at the board level in terms of what the company decides to do. So, we can make sure the cash is utilised for the right purposes, for example. The other thing is that we invest with a strong and like-minded syndicate so that we have the collective wisdom of the entire syndicate, as opposed to relying on ourselves to see an investment through.

“We pride ourselves on our vigorous investment decision process. So, we kind of manage the risk at the point Of entry itself. For example, we have an internal adviser that looks at a particular area that he or she may have the experience and expertise in. Then [we add an additional] layer with an external specialist who really looks at the technology itself and does a detailed technology review of a particular company.”

He adds that Xeraya also incorporates peer reviews into its deals to ensure that the right structure has been put in place to manage the various risks. However, despite the stringent due diligence, some investments are bound to fail. This could happen to even the best of investors, he says.

“Looking at a company and actually executing an investment are two different things,” says Fares, stressing that this is the reason the firm imposes such a stringent due diligence process.

One of the recent scandals in this field has been the failure of US-based health technology company Theranos Inc. Founded in 2003, the company raised more than US$700 million from venture capitalists and private investors, resulting in a US$10 billion valuation at its peak in 2013 and 2014. The company claimed that it had devised blood tests that only needed small amounts of blood compared with what was ordinarily needed and cost far less than existing tests.

However, in 2015, its claims were challenged by medical research professors John Ioannidis and Eleftherios Diamandis. The story was broken by The Wall Street Journal’s investigative reporter John Carreyrou. Theranos and its founder, Elizabeth Holmes, are currently facing a string of legal and commercial suits.

“If we look at the [Theranos] claims, investors never actually opened the box, so to speak. For us, we need to see the box, open it and evaluate the thing in it before making an investment,” says Fares.

He adds that the pricing of companies is an important factor in Xeraya’s investment decisions. From a valuation perspective, he says, much of the geopolitical risks such as the US-China trade war and the US presidential election in November appear to have been priced in.

“In pharmaceuticals, we will probably invest in early-growth-stage ventures, where people are not thinking about the pricing of drugs just yet because they are still thinking about the development of the technology, as opposed to the marketing of the technology itself or the approval of the drug,” says Fares.

“We will also invest in areas where the platform technologies are quite active. For instance, in the oncolytic virus space, where even with failed pre-clinical or clinical kind of data, [the technology] can be acquired at nice valuations.”

Oncolytic viruses are highly efficient at killing tumour cells in vitro, especially in a two-dimensional monolayer of tumour cells.

“I think the simplest way to look at the various segments in terms of why it would be an attractive investment is by asking ourselves, which are the large companies today? And then take a step back and look at the types of large com-panies 10 years ago,” says Fares.

“The top five largest companies 10 years ago were probably oil and gas companies and banks. But today, the top five largest companies are tech players such as Apple, Facebook and Alibaba.

“Why is this the case? Some would argue that it is because tech companies have this inherent ability to programme things. Hence, it is easier to scale a business in tech than in other sectors.

“What about the next 10 years? Is there a particular sector that has similar characteristics? Some would argue that life sciences are at the cusp of similar transitions.”